The boomerang effect: sanctions are hurting the West more than Russia.

The West imposed extreme sanctions on Russia in the first week of the war in the hope that they would bring Russia's economy to its knees and make it impossible for the Kremlin to pay for Putin's war. Not only did it not work, but sanctions have been bouncing back in a boomerang effect on the EU. / bne IntelliNews

After two years of war in Ukraine, the sanctions regime has run its course. As sanctions rules are tightened they are starting to boomerang back and are increasingly hurting Europe more than they are Russia.

The extreme sanctions imposed on Russia in the first days of the Ukraine invasion were designed to collapse the Russian economy at best, or at least throw Russia into a crisis that would make it impossible for Russian President Vladimir Putin to fund his war.

It didn’t work. Russia came close to a meltdown in March and April 2022, but the team at the Central Bank of Russia (CBR) acted fast and efficiently headed off a disaster with strict capital controls and banning withdrawals of dollars. Crucially, the EU continued to send billions of dollars to Moscow every month to pay its gas bill, throwing Russia a key lifeline. That was a mistake.

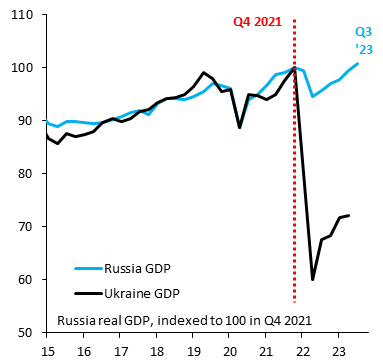

As 2023 comes to an end it is now clear that Russia’s economy has proved to be a lot more robust than thought, says political economy analyst Alexandra Prokopenko. GDP will expand by 2.2% this year. Growth is so strong in many sectors there is talk of overheating. The budget is back in profit. Both Russia’s oil revenues and its nominal GDP are back above the level they were on the eve of the invasion over 600 days ago.

“Russian real GDP is above where it was before the invasion. That is lamentable, but no one in Brussels gets to lament this. The EU made a conscious decision to put the profits of a handful of Greek shipping oligarchs ahead of the 450mn people it’s supposed to represent,” said Robin Brooks in a bitter tweet, the chief economist at Institute of International Finance (IIF), referring to Greek shippers that have largely ignored sanctions to make money by shipping Russian oil to Asia.

One of the miscalculations the West made was to underestimate the quality of the financial and macroeconomics team running the economy. As Prokopenko points out, these people have been in charge of these policies since the 2008 credit crunch and are crisis veterans. Underpinning this resilience is a mindset of “permanent war”, reminiscent of the totalitarian regime described in George Orwell’s novel 1984. They have had to deal with one disaster after another, which left them uniquely prepared to fight the latest clash with the West.

“The succession of crises has instilled a particular mindset in Russian officials. The perpetual need to address challenges that arise from factors beyond their control, often unrelated to monetary and fiscal matters, has kept them in a state of constant readiness for unexpected crises. This mindset, coupled with substantial oil revenues, has enabled the Russian economy as a whole to withstand the impact of sanctions and swiftly adapt to new realities. The role of crisis management by the central bank and the finance ministry in responding to sanctions should not be underestimated,” says Prokopenko, in the preamble to her report.

On top of that, it appears that Putin has been preparing for the current showdown for over a decade, building a Fiscal Fortress with massive reserves and low debt that has largely sanction-proofed Russia Inc.

By contrast, Europe is not good at dealing with crises. Almost all the EU members saw negative growth in the third quarter according to the latest OECD data and the forward-looking S&P Global Production Manufacturers Index (PMI) for October remains deeply in negative territory, while industrial production in many countries is sinking.

As bne IntelliNews reported already last year, the lights are going out in Europe’s heavy industry after input and power prices rocketed. German industrial powerhouse BASF has been forced to shutter or dramatical reduce production at hundreds of factories across Europe due to unaffordable energy and gas costs which has made them economically unviable. By some estimates 10% of Germany’s heavy industry has been mothballed.

As bne IntelliNews has reported, sanctions across the board have failed to have the intended impact. Oil sanctions are now a spent cannon and technology sanctions have failed thanks to Russia’s long list of friendly countries that are making a killing from transiting banned Western goods to Moscow.

The EU is currently debating the details of a twelfth sanctions package, which are supposed to tighten the sanctions regime and improve enforcement, but there is already stiff resistance to tightening the noose amongst many EU member states because of the painful economic bounce-back effects.

Russia is too big, too autarkic and too deeply embedded into the global economy to be effectively sanctioned. The Fiscal Fortress Putin has built since around 2012, still has some $300bn in cash (mostly yuan and gold) despite the freezing of the CBR reserves, and only 14% of GDP of state debt – by far the lowest level of any major country in the world.

There are too many emerging Global South markets that are too big, growing too fast and too independent of Western pressure that are willing to trade with Russia to allow the West to effectively enforce the sanctions. After the EU banned Russian oil imports in December 2022, Russia was able to reorientate its entire oil exports to Asia in a matter of months.

While Russia is still getting the foreign-made machinery it needs via the backdoor, Europe remains heavily dependent on many critical inputs it can still only get from Russia. Europe suffers from a deficit of energy, metal, food and chemicals and as it has started to de-industrialise it has become more dependent on Russia than ever. Things like Russian fertilisers, LNG, gas and grain all remain unsanctioned for this reason.

“This theme is nothing new,” said presidential spokesman Dmitry Peskov in November, when asked about the twelfth sanctions package.” This is a continuation of the search for some kind of sanctions solution, which, according to the authors of these sanctions, will hit Russia. As a rule, it turns out to have a kind of boomerang effect. The interests of Europeans suffer.”

Europe goes into recession

Global growth will fall from 6% in 2021 to under 3% this year, says the World Bank, but that is not all due to the boomerang effect. The polycrisis, persistently high food inflation and rising energy costs, the deglobalisation that followed the pandemic and the increasingly fractured world that is a result of the trade disputes between the US and China before the Ukraine war have all taken their toll. But the boomerang effect has catalysed all these problems and hit Europe particularly hard.

The economies of Central and Northern Europe are spluttering and Germany, the engine of European growth, has stalled completely. Germany ranks bottom for business confidence in Europe, according to the latest S&P Global Business Outlook survey. Firms are forecasting cuts to both employment and investment and staff cost pressures expected to remain high for at least the next year. And its economy contracted in the third quarter as it slips into recession.

Economists are calling Germany “the Sick Man of Europe” again, although Czechia also has a strong claim to that title, as it is the only economy in Europe not to have regained its pre-pandemic size and is also bottom of the growth table. Hungary and Poland are also recovering from bouts of inflation that have been the highest in 20 years.

But the picture is very similar across most of Western Europe, although the countries of Southern Europe are faring better. The business climate in France deteriorated again in November and growth is anticipated to slow further in the fourth quarter. At the same time, the PMI indices indicate that inflationary pressures remain high and that disinflation will take time, according to ING.

The European Commission said in its Autumn Economic Forecast that energy prices remain a problem and revised down its forecasts for GDP growth in the EU and in the eurozone this year, by 0.2 percentage points to an average of only 0.6% this year before recovering slightly in 2024 to 1.3% growth. All of Austria, Czechia, Estonia, Germany, Hungary, Ireland, Latvia, Lithuanian, Luxembourg and Sweden will see their economies contract this year, but all, except Sweden, are expected to put in at least some anaemic growth next year.

“EU GDP growth is forecast to improve to 1.3% in 2024, still below potential and a downward revision of 0.1 pps. from summer. It is projected to gain further pace, to 1.7%, in 2025,” the EC said in its report.

More generally, the World Bank says global growth is forecast to slow from 6.0% in 2021 to 2.7% in 2023 before recovering a little in 2024 to reach 2.9%, which is being driven by the polycrisis.

The EC said while inflation in Europe is declining from 20-year highs in some European countries, the monetary policy put in place to control it, “took a heavier toll than previously expected” this year and another lacklustre quarter ahead. Some Central European banks are getting ready to ease monetary policy, but the European Central Bank (ECB) has made it clear in comments that growth-boosting eurozone rate cuts in 2024 are unlikely.

The European slowdown is not a disaster yet. ING called it a “very shallow technical recession” in a note on November 23 and suspects the low point has already been passed. But against that, analysts say that climbing out of the bowl will take several years. The bottom line is that the anaemic eurozone economies are currently in a lot worse shape than Russia for the meantime.

Poor PMIs

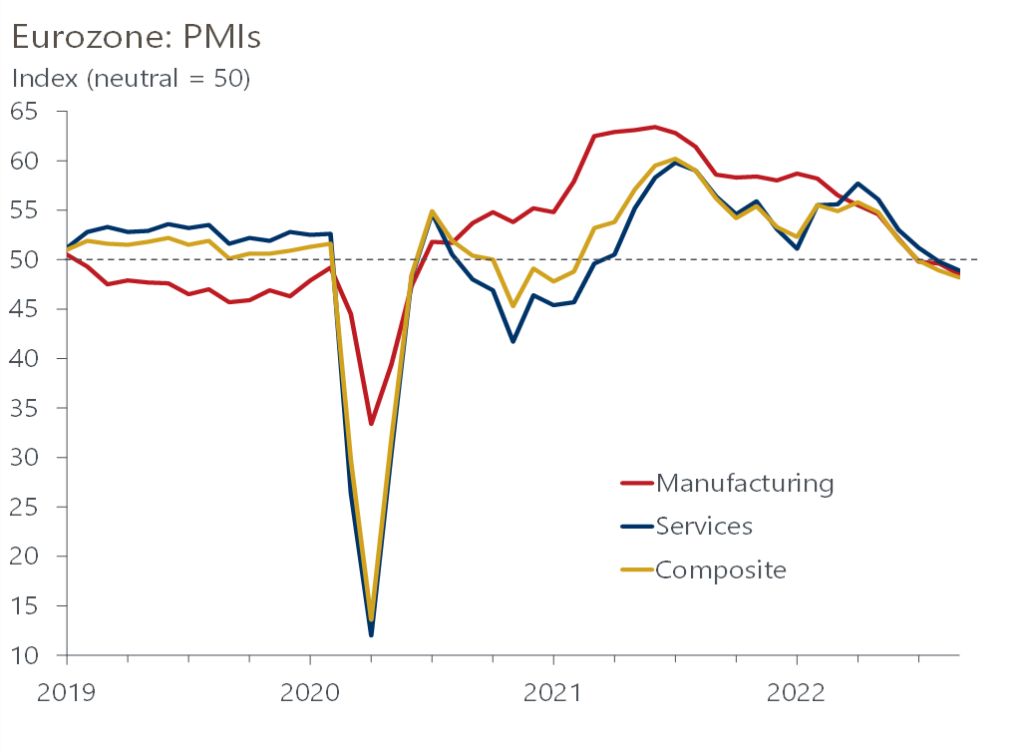

Capital Economics says that Europe is facing a “long slog” and following on from the GDP contraction recorded in the third quarter, monthly indicators suggest the economy is likely to remain in recession in the fourth quarter.

“The outlook for European manufacturing in general looks bleak,” says Liam Peach, an emerging market economist with Capital Economics. ING points to the poor PMI results as a warning sign, where any result under the no-change 50 mark is a contraction.

“The eurozone composite PMI ticked up from 46.5 to 47.1 in November, which still indicates a contraction in business activity. New orders continue to fall as backlogs of work are being depleted. This is more so the case for manufacturing, where the downturn is deeper than for services… The downturn is not worsening at the moment, but there is little evidence of recovery either. Overall, it looks like this is a shallow technical recession.” ING said in a recent note.

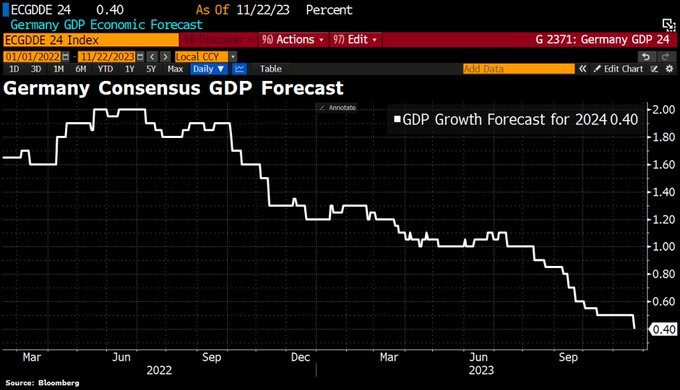

Germany is key to a recovery and currently the country is one of the worst performing of all big EU states. And now it is facing a spending squeeze.

The German budget was thrown into chaos in November after the Constitutional Court ruled that Chancellor Olaf Scholz could not transfer €60bn of pandemic relief money to the climate crisis investment fund, and the state has had to put all new spending plans in 2024 on hold as a result. Now strapped for cash, that will hurt growth prospects even more.

“The growth forecasts for 2024 have been cut following the budget chaos after the Constitutional Court declared [the] government’s spending plans unconstitutional. The consensus now expects GDP growth for Germany of just 0.4% for the coming year,” Holger Zschäpitz, a journalist with Die Welt, said in a tweet.

Germany’s budget woes may also affect its funding for Ukraine as the EU overtakes the US as the biggest Ukrainian donor. Berlin says it will continue to support Kyiv despite budget difficulties, but it will have to take funds from non-military budget items and tighten its belt.

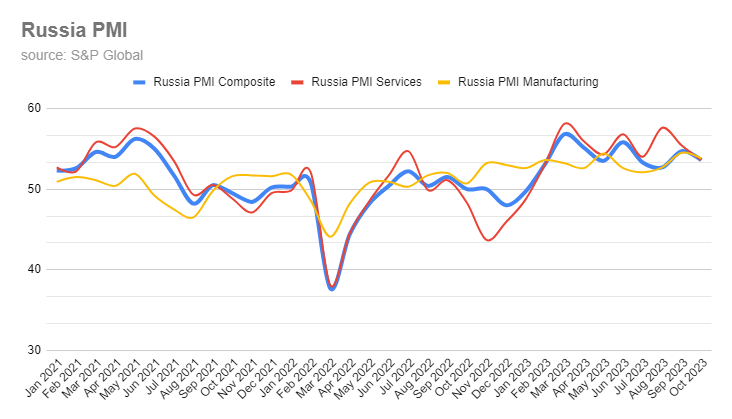

Russia’s PMI, on the other hand, is booming. It put in the biggest jump in five years to 54.5 in September thanks to the military Keynesianism boost of heavy military spending, and has shown economic expansion every month this year. Russia’s PMI remained a robust 53.8 in October and Russia’s businessmen are optimistic about the prospects for the near term. (chart)

The story is the same with industrial production. Germany and France are both in the red compared to 2015, and the UK is headed for stagnation in 2024, due to high interest rates, according to ING.

Spain was the only EU economy to see industrial production rise in September but by only 0.6% year on year. September was the weakest month of German output compared to 2015, and Dutch manufacturing output has fallen every month so far in 2023, plunging by 10.3% in October alone.

Industrial production in Russia is back in the black since the war started and showed a modest uptick in growth in September, rising from 5.4% y/y in August to 5.6% y/y. (chart)

EU economic slowdown straining relations between EC elite and sovereign member states

In the days following the start of the war European Commission President Ursula von der Leyen was a unifying force and looked like “the new Merkel” as she rallied the EU members to impose crushing sanctions on Russia.

But since then she has started to look more like an ideologue, hell bent on crushing Russia at all costs – including at the cost of the economic health of the EU countries. Von der Leyen has come in for criticism for her total lack of condemnation of Azerbaijan’s so-called anti-terrorist operation and the ethnic cleansing of the Nagorno-Karabakh enclave on September 19 – clearly an EU values issue. Her willingness to completely ignore Azerbaijan’s atrocious human rights record when cutting a gas deal with Baku last year has also been roundly criticised. And her blatant pro-Israeli support led 800 members of her staff to publish a letter of complaint.

Now tensions are rising between the EC’s tough line on Russia and what the member states desire to protect their economies.

Sanctions have cost Europe a lot. Sanctions were first imposed in 2014, following the annexation of Crimea, and have hit Europe disproportionately, as the US has little trade or investment in Russia. In dollar terms, the European Union economy is now 65% of the United States economy, according to the FT, down from 91% in 2013. In addition, American GDP per capita is more than twice that of Europe, and the gap continues to widen.

Some EU member states are attempting to protect already damaged sectors while politically supporting the punishment of Russia. The eleven rounds of sanctions are riddled with exemptions and calve-outs to protect some of the more vulnerable industries, and everyone in Europe has been indirectly affected by the soaring energy prices and sky-high inflation.

As bne IntelliNews reported a year ago, the lights are starting to go out in Europe as just the soaring energy costs in Europe and lack of gas have already forced companies like Germany’s industrial powerhouse BASF to shutter or drastically reduce production at hundreds of factories in Europe that are unlikely ever to reopen. Germany’s heavy industry has already been reduced by 10%, according to some estimates. Energy prices have come down from their extreme levels in 2022, but they remain 2-3 times above the pre-war five-year averages and continue to punish European industry.

The cost of power has become a new tax that is also dragging down growth and investment. Households in Belgium and Germany are already paying twice as much for electricity as Poland, a German government research body said in November. Energy price rises have particularly squeezed small to mid-sized homes in the two countries in the first half of 2023, despite falling from astronomically high levels in 2022.

The German government is planning to spend billions of euros on subsidies to shelter the population from the high prices for at least the next four years, but its budget is already being squeezed as it hits Constitutional borrowing limits, known as the “debt brake”, in the middle of November. A recent German study found that two out three companies operating in Germany are now looking to relocate at least some of their operations abroad to save money.

And a lot of money has been spent. The US reportedly made over $1 trillion in excess profits from LNG exports to the EU last year in the midst of the energy crisis that saw prices decuple. The EU reportedly lost €1 trillion through hand outs and energy subsidies to protect households from the worst: governments provided $830bn to assist consumers and another $446bn to fossil-fuel producers, many of whom recorded bumper profits.

Western governments can’t keep that level of spending up. The US is reportedly planning to end energy subsidies this winter and will pass more of the costs on to the consumer. UK regulator Ofgem has raised the national price cap for the first quarter of next year by 5% at a time when Britons are facing persistent inflation in the price of food and basic goods, and the government is struggling with worsening economic growth forecasts.

Likewise, Germany’s €200bn fund to soften the impact of rising energy prices on consumers and businesses will expire at the end of 2023, Finance Minister Christian Lindner told Deutschlandfunk at the end of November. “As of December 31 of this year the Economic and Stabilisation Fund will be closed,” he said in a recent interview. “There will be no more payouts from this. The electricity and gas price brakes will also be terminated.” The fund, known by its German abbreviation WSF, is one of the off-budget funds ruled unconstitutional by the country’s highest court in the middle of November.

Twelfth package of sanctions

The tensions between government’s desire to protect their struggling industries and the EC’s determination to do Russia in has come to a head with the twelfth sanctions package, now under discussion.

The details were due to have been announced on November 17, but this has now been delayed to sometime in mid-December as the intra-EU wrangling becomes fraught.

The latest package is designed to better enforce the existing sanctions, which have largely failed to inflict much pain on Russia. As bne IntelliNews has extensively reported, Russia has managed to avoid almost all the sanctions, which have done little more than impose some extra costs on its trade. Oil sanctions are a spent cannon and the FT reports that not one barrel of oil has been sold below the $60 per barrel oil price cap. Technology sanctions have also failed thanks to the co-operation of Russia’s friendly countries; to illustrate, German exports to Kyrgyzstan alone, especially of cars, are up by 5,500% since the start of the war.

Kyrgyzstan has become a key destination for all European exports that – ultimately – go to Russia. Estonian exports to Kyrgyzstan are up 10,000%. Finnish exports are up 3,100%, Poland’s are up 2,200% and Greece’s are up 2,100%, IIF reports.

More insidious are reports that Turkish exports of dual-use goods to Russia were up three-fold in 2023, the FTreported on November 27. Turkey recorded $158mn in exports of 45 goods like microchips over the first nine months of 2023, marked by the US as sensitive to Russia and five “former Soviet countries” suspected of serving as intermediaries for Moscow. The average figure for the trade of the same goods in 2015-21 was $28mn, according to the FT.

The new package is supposed to tighten the noose and will impose new regulations, reporting and fines on European companies that break the rules. However, Bloomberg reported on November 24 that several EU members are already pushing back hard, as they don’t want to punish their own companies for Russia’s wrongdoing. They also don’t want to forgo the money they are making.

The EC is proposing to prohibit importers from reselling many goods, in particular, semiconductors used in Russia for the production of weapons. It is also proposing to fine EU countries that ignore the rules and put the money in a special “Ukraine Recovery Fund”. Exporters will also be required to inform national authorities of any violations by third-country companies.

However, diplomats from an unnamed group of major EU member states raised several “concerns” about the proposals in the last week of November, including questions about their legality and whether such guarantees and conditions could be demanded from importers.

Bloomberg’s sources said that the group of countries want to narrow the scope of the proposed rules, reduce the list of goods to which the new laws will apply and introduce more exemptions and calve-outs that have already fatally weakened the existing sanctions regime. They are afraid the rules will place them at a “competitive disadvantage.

The problems that arise from on the one hand sanctioning Russia’s biggest export earners and the losses to European firms using or buying those products are thrown into relief by the proposed bans on diamonds and aluminium.

Diamonds: Russia is one of the world’s biggest producers of diamonds in the world and accounted for 35% of the world’s trade in 2021, worth $4bn. Belgium buys up to half of Russia’s diamond exports, 28.2mn carats, worth approximately $2.5bn in 2021, according to Kimberley Process data, which are sold in Antwerp. Unhappy about losing this significant trade, Belgium has successfully kept diamonds off the sanctions lists until now, but diamonds are likely to be included in the twelfth sanctions package.

Typically, the ban on imports of Russian diamonds to the EU will come into effect immediately on January 1, but the wider ban on goods produced using Russian diamonds and stones cut elsewhere, like India, will be phased in over a year to ease the pain on Antwerp.

Aluminium: Russia is an equally important producer of aluminium which has also been excluded. A previous attempt to sanction the oligarch owner RusAl, Russia’s main producer, Oleg Deripaska in 2018 backfired when the price of aluminium spiked by 40% the next day on the London Metal Exchange (LME). The US Office of Foreign Assets Control (OFAC) backed off when it was told the cost of a can of Coke in the US would rise by 15 cents and the sanctions were eventually withdrawn entirely – the only sanctions imposed on Russia since 2014 to have been withdrawn again.

Aluminium products are back on the lists again. The twelfth sanctions package reportedly includes wire and pipes, but that has caused an outcry from the Federation of Aluminium Consumers in Europe (FACE) that warned the ban will cause chaos amongst European businesses that rely on Russian aluminium.

“Aluminium was the target of a vigorous and persever[ing] lobbying campaign from competitors of Russian producers and some industry associations, and it finally made its way up to the Commission’s proposal for the 12th EU sanctions package,” FACE said in a statement.

Europe already has a net deficit of primary aluminium, now at more than 84%, according to FACE. Nobody foresees any new smelting production investments on the Continent, and the most optimistic recycling scenario will at best cover half of the demand for this ever more sought-after material, according to the consumer’s association, which warns of business-busting price hikes.

Grain & trucks: A more recent example of unintended consequence has been grain exports from Ukraine. The major foreign exchange earner for Ukraine, its grain has been bottled up since the Black Sea Grain Initiative collapsed in July.

Ukraine redirected its exports by rail via Poland, but massive quantities of cheap low-quality Ukrainian grain crashed the local market in April and the transit of Ukraine’s grain has been banned ever since.

More recently, a new trade dispute has broken out after Polish truckers blockade the border to prevent Ukraine’s trucks from crossing. Already smarting from the loss of business ferrying EU goods to Russia, Poland’s truckers are complaining Ukrainian truckers, who earn a quarter of what Polish truckers do, are undercutting them and putting them out of business. This dispute is also spreading to Poland’s neighbours in adjacent Central Europe.

Determined to support Ukraine, even at the expense of hurting Poland, the EC has refused to reinstate the permit restrictions on Ukraine’s truckers that was rescinded last year, and Warsaw has refused to lift the ban on Ukrainian grain imports, as it is Brussels, not the member states, that makes trade policy.

Czech steel: Another less celebrated example is Czech steel companies, which have asked for an extension to exemptions from a ban on buying Russian steel. Novolipetsk (NLMK) is one of Russia’s biggest steel producers, but has rolling mills in Europe in order to be close to its big customers.

Czechia’s automotive sector is a linchpin for the economy, accounting for about 10% of national GDP – one of the highest totals in the world – and is heavily dependent on the import of Russian steel which is used to make the car bodies.

NLMK produces nearly all of its flat and long steel products in Russia, but nearly a quarter of its rolling operations are sited in Europe and these products were included in the eleventh sanctions package. Czechia got an exemption which is due to expire next year. In addition, thousands of European jobs at NLMK’s European plants are on the line. Czechia is now asking to prolong that transition period to 2028. Belgium is likely to support Czechia’s call for an extension, as it is also home to a large NLMK steel mill.

Exodus: Just how badly Germany’s economic model has been affected by the end of cheap Russian gas remains a matter for debate, but clearly the costs of energy have risen dramatically and are unlikely to return to the pre-war long-term averages anytime soon. That has made a swathe of German businesses economically unviable.

Manufacturing accounts for more than a quarter (27%) of the German economy. New orders at the country’s engineering companies, long a bellwether for the health of Germany Inc., have been dropping like a stone, falling 10% in May alone, the eighth consecutive decline. Foreign direct investment (FDI) into Germany is also collapsing, down in 2022 for the fifth year in a row, hitting the lowest point since 2013. German firms are already looking for new homes, a recent study by the Federation of German Business (BDI) found.

Already 16% of the medium-sized companies interviewed by the BDI have launched steps to relocate parts of their business abroad, but the study found that another 30% are actively studying relocation options. The German government is planning a major four-year €4.4bn subsidy programme to keep German businesses at home. If Germany’s deindustrialisation continues then it will have Continent-wide ramifications.

“Almost two-thirds of the companies we interviewed consider prices of energy and resources to be among the most pressing challenges,” said BDI President Siegfried Russwurm, as cited by Euroactiv.

German industrial giant BASF, founded on the banks of the Rhine in 1865, has just decided to forego a $10bn investment in a new chemical plant in Germany, choosing to locate it in China instead. As bne IntelliNews reported last year, BASF has already shuttered hundreds of factories and plants in Europe as a result of soaring gas and energy prices.

In the most recent example, Germany’s biggest solar panel maker, Meyer Burger Technology, is contemplating relocating its operations abroad due to the energy crisis. The CEO, Gunter Erfurt, said a decision would be made soon, citing the difficult power situation in Germany as a potential reason for the move, Brussels Signal reported. The United States is a possible new location, encouraged by substantial government investment in the solar sector and offers of significant state support for the company’s already planned manufacturing plant in the US.

Sanctions are distortions

Oil sanctions won’t work unless Russia is totally encircled and all Russia’s exports have to leave through a gate that is controlled by the West, which then can enforce the $60 per barrel rule.

When the oil price sanctions were first suggested, as the West controlled 95% of maritime insurance it was assumed this could serve as the enclosing fence. The flaw in the scheme is that the entire eastward facing export route is wide open, allowing Russian ships to sail to Asia totally avoiding the Western controlled gate entirely.

Chinese and Indian shippers have their own insurance and have refused to participate in the scheme in exchange for cheap Russian oil. At the same time Russia has built up a “ghost fleet” of ships that can carry almost all its own crude that operates entirely outside of the sanctions regime. After two years, the West is estimated to now control some 65% of the global maritime insurance business.

The US has imposed secondary sanctions on a total of five shipping companies in November and is investigating 100 more for ignoring sanctions. Western companies have been widely ignoring the regime with impunity, as detailed in an investigation by The Peterson Institute for International Economics (PIIE) and Kyiv School of Economics (KSE). In another note KSE warned that oil sanctions are in danger of losing their credability as they are working so badly.

The West is increasingly being sucked into a game of whack-a-mole to make leaky sanctions work. It is targeting individual ships and companies after the much more elegant market mechanism of using insurance to enforce the rules continues to fail. Without nailing all the holes shut – sanctioning both China and India for example – you can’t win whack-a-mole and that would mean sanctioning the whole of the non-aligned world.

The hole in the eastern side of the ringfence means that sanctions are not sanctions but a distortion of the once highly efficient global energy market. Whereas once Russian oil from Siberia had to be shipped from Primorsk in the Gulf of Finland a few days to the oil terminals in Rotterdam where it was refined before being distributed across Europe, now it has to sail for two months to Indian refineries in Gujarat or Chinese privately owned “teapot” refineries, before being shipped back to Europe and sold as “Chinese” or “Indian” oil products. It is of course the same Russian oil, except it has been whitewashed by the journey. Ultimately, it is the European customer that pays the added transport costs.

As the roundtripping Asian trade route becomes well established, the discount Russia had to offer has been falling steadily according to the latest KSE Russian oil tracker. Pre-war the Urals blend was sold at a $2 discount to Brent. At its peak in the spring of 2022 that discount blew out to some $35, but since then it has fallen to $10 now and analysts expect it to fall further next year to $5, reflecting the longer journeys involved.

The upshot of the hole in the ringfence, combined with the agreement between Russia and OPEC+, led by the Kingdom of Saudi Arabia (KSA), now a firm Russian ally, to restrict oil production, has been to push up the price of crude to over $80 per barrel, which more than compensates for any increase in transport costs.

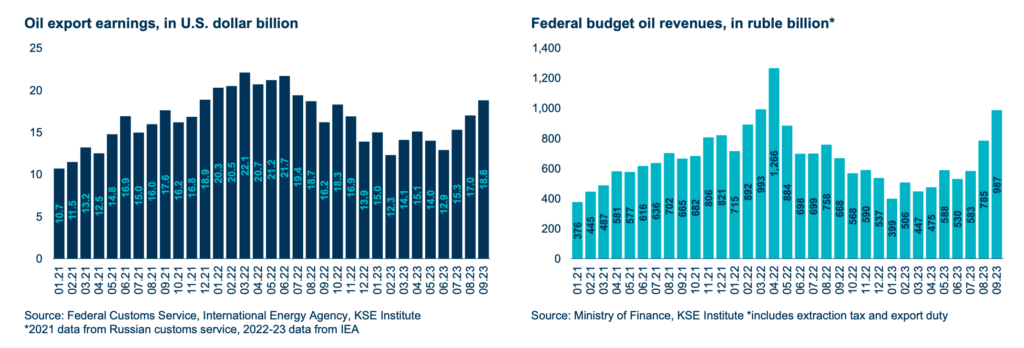

The distortions that have been introduced into the oil markets is one of the main mechanisms for the boomerang effect. In February 2022 on the eve of the war Russia earned $20.5bn from oil exports and the budget received RUB892bn ($10.7bn), according to KSE. In September this year Russia earned $18.5bn from oil exports in dollar terms and RUB987bn ($11.1bn) using the exchange rates current at the respective times. Instead of dramatically reducing the amount of money the Kremlin gets to fund its war machine, it is now earning more than it did in January 2022.

Cost to Russia

That is not to say the sanctions are useless. They have done a lot of damage but more importantly they condemn Russia to long-term stagnation. Thanks to Putin’s efforts to build a Financial Fortress, Russia’s growth potential pre-war was only 1-2% a year – far below the average global growth rate, condemning Russia to long-term stagnation in the long term. Prokopenko argues that the “permanent war” mentality of Russia’s financial elite leads to hoarding of resources, super-conservatism and discourages institutional building, long-term investment or planning and stifles innovation. Following the sanctions, Russia’s growth potential has fallen to a mere 0.3-0.5% as a result, say economists. That’s stagnation.

But Ukraine can’t wait for the long term. It needs results now after the much vaunted summer counter-offensive led to a stalemate which is fuelling the already palpable Ukraine fatigue.

Apart from slow growth, the most obvious cost to Russia has been the collapse of bilateral trade between Russia and the EU, formerly Russia’s biggest trade partner. Trade with China has more than doubled in the same period and is on course to top $200bn this year, but that doesn’t come close to replacing the trade lost with the EU.

After a slowdown in trade between 2013 to 2016 caused by the first round of sanctions, Russo-EU trade recovered rapidly in 2017 according to the Russian customs to just under €250bn and stayed pretty constant at that level until 2021. In this period Russia was running an annual trade surplus with Europe on the order of €80bn a year of which over a third were oil and gas in value terms.

In 2021, the total trade in goods between the EU and Russia amounted to €257.5bn, according to Eurostat.

The EU’s imports were worth €158.5bn and were dominated by fuel and mining products – especially mineral fuels (€98.9bn, 62%), wood (€3.16bn, 2.0%), iron and steel (€7.4bn, 4.7%) and fertilisers (€1.78bn, 1.1%).

The EU’s exports in 2021 totalled €99.0bn. They were led by machinery and equipment (€19.5bn, 19.7%), motor vehicles (€8.95bn, 9%), pharmaceuticals (€8.1bn, 8.1%), electrical equipment and machinery (€7.57bn, 7.6%) and plastics (€4.38bn, 4.3%).

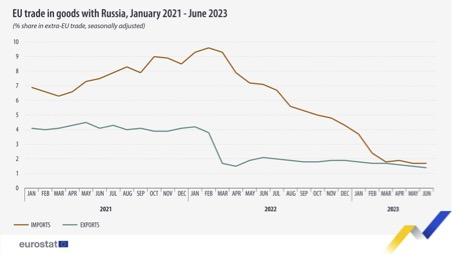

But in 2022 most of Russia’s leading export products were sanctioned and by the start of 2023 all oil and gas imports stopped entirely, cutting just under €100bn out of mutual trade by themselves. The Russo-EU trade turnover halved to €171.4bn in 2022 as EU exports fell by a third to around €40bn, even though Russian exports to the EU were up two thirds to €137bn in value terms (due to the energy crisis).

Trade between Russia and Europe this year is down more than 3-fold after EU exports to Russia fell to under 2% of total EU trade in the first nine months of this year, from 9.6% in 2022 in the same period, according to Eurostat. The EU now runs a trade deficit with Russia of only €400mn a month or less, down from the pre-war average of about €8bn a month. Russia’s mutual trade with the EU is on course to fall below €100bn this year.

Russia’s growth of 2.2% this is an aberration caused by the military spending, but once that wears off the economy will stagnate.

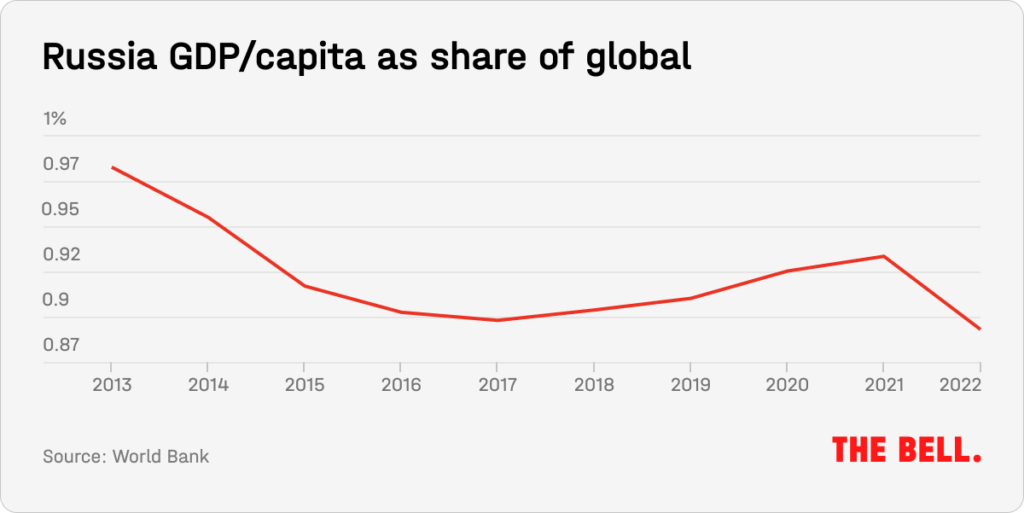

Russia’s share of GDP/per capita as a share of the world is already falling, reports The Bell. Since 2013, Russia’s GDP per capita has only increased by 5%, which is lower than the world average and most developing countries. Prior to the Ukraine conflict, Russia’s GDP per capita was just 2% below the global average, but this gap has now widened significantly.

The annexations of Crimea and four more Ukrainian regions last September are also a heavy burden as they are amongst the most heavily subsidised regions in the Federation.

And all this is not counting the cost of the war itself. In Russia’s 2024 budget the Kremlin is for the first time ever spending more on security than on social spending. This year Russia is expected to spend RUB15 trillion on the war ($168bn), or some 10% of GDP.

“Expenditure on this scale leads to the expansion of groups that benefit from war (soldiers and their families, the military-industrial complex, military officials) and a reduction in income for everyone else. Extending the war will result in a gradual decline in living standards in Russia,” the Wilson Centre said in a recent note.

Donald Trump Should Not Repeat Woodrow Wilson’s Failure

April 30th is an important date in American politics. This is the day 100 for the American President in the White House, and all attention will be on the reports of his achievements and failures. But nothing can be more critical than Peace…

○

6 mins read

A Holocaust perpetrator was just celebrated on US soil. I think I know why no one objected.

Russia’s invasion has made ordinarily outspoken critics of antisemitism wary of criticizing Ukrainian Nazi collaborators

○

1 min read

Qi Book Talk: The Culture of the Second Cold War by Richard Sakwa

Richard Sakwa has for many years been one of the most distinguished and insightful observers of relations between the West and Russia, and one of the leading critics of Western policy. In this talk with Anatol Lieven, director of the Eurasia program at the Quincy Institute, Sakwa discusses his book, The Culture of the Second Cold War (Anthem 2025). The book examines the cultural-political trends and inheritances that underlie the new version of a struggle that we thought we had put behind us in 1989. Sakwa describes both the continuities from the first Cold War and the ways in which new technologies have reshaped strategies and attitudes.