The boomerang effect of the Russian sanctions on the EU member states is having a mixed impact. Germany, France and Italy are worst affected as the pain from the changes in energy and input supplies impact their economies, dragging them down into recession, while the less dependent on Russia like Spain and Portugal are already showing signs of recovery, according to ING analysis.

The boomerang effect of the Russian sanctions on the EU member states is having a mixed impact. Germany, France and Italy are worst hit, but even those doing better are facing litle more than stagnation in 2024, says ING. / CC: bne IntelliNews

Overall Europe is headed for a year of stagnation that could be worse than in 2023. By contrast Russia reported growth of 3.5%, according to the preliminary results. And on January 18, an ebullient Russian President Vladimir Putin said that growth could come in at over 4% after revisions. The Russian Ministry of Finance (MinFin) also revised its GDP growth outlook for 2024 up to 3.5%, much improved from the earlier Central Bank of Russia (CBR) forecasts of around 2% for this year.

Currently, sanctions seem to be doing more harm to Europe than they are to Russia.

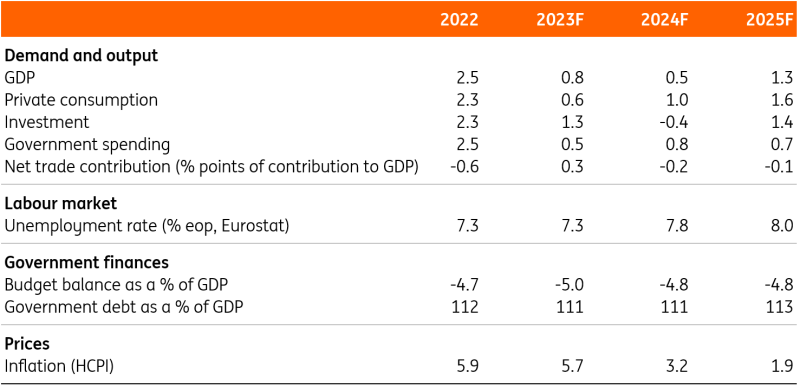

Germany: Farmers’ protests, train strikes and disappointing macro data from the first weeks of the new year did not wash away a disappointing 2023, in which the economy contracted by 0.3% y/y. “In fact, it looks like the German economy has entered another challenging year of stagnation and political turbulence,” ING said in a note.

Germany’s economy was already struggling before the war in Ukraine broke out, including supply chain frictions resulting from the pandemic made worse by the war in Ukraine, an energy crisis, surging inflation, and a tightening of monetary policy that have led to economic stagnation.

“Looking ahead, at least to the first few months of 2024, many of the recent drags on growth will still be around and will, in some cases, have an even stronger impact than last year,” ING said. “We expect the German economy to shrink by 0.3% y/y this year. It would be the first time since the early 2000s that Germany has gone through a two-year recession, even though it could prove to be a shallow one.”

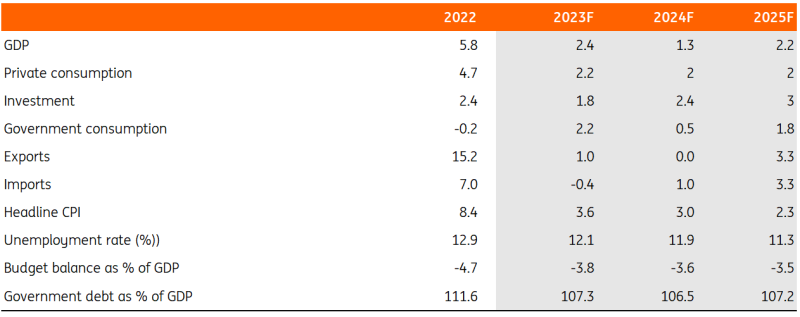

France: The French economy is likely to remain very sluggish at the start of 2024, before picking up a little more momentum in the second half of the year, although growth is likely to be weak and below the consensus forecasts, said ING in a note.

“The economy appears to be stabilising, but activity is subdued. And that means the country will probably escape a prolonged recession,” ING said. “Persistently high inflation (3.7% in December), the very negative impact of restrictive monetary policy on investment and the construction sector, the slowdown in the global economy and the geopolitical risks weighing on confidence will continue to be a drag on the French economy. Weak growth of 0.1% is expected for the first quarter.”

Over 2023 as a whole, French GDP will have grown by around 0.8% after the dynamic recovery of 2022 (+2.5% over the year).

Inflation should continue to fall in 2024, although not as quickly as in other European countries. As inflation falls, ING expects real purchasing power to pick up again, with wages expected to rise more strongly than prices. This will enable consumption to contribute more to French economic growth than in 2023. As a result of weaker demand, job losses and a moderate rise in unemployment are expected over the coming quarters, which will limit the pace of the recovery.

ING expects GDP growth to be on the weak side in 2024, averaging 0.5%. In 2025, growth should pick up to around 1.3% for the year.

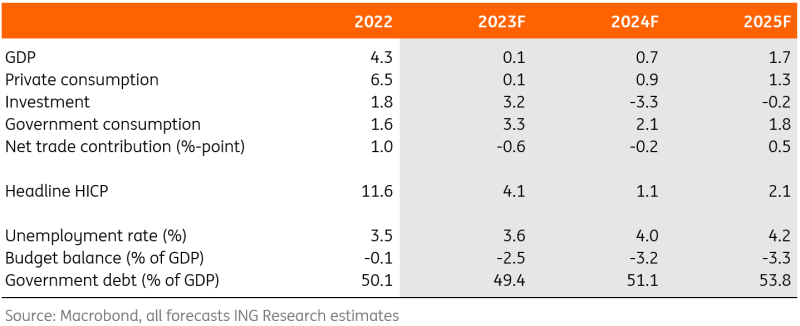

Italy: As the impact from any upcoming monetary easing will be only gradual, Italy’s growth profile over 2024 will also depend on how fast and effective the investment leg of the EU recovery plan will be.

The restrictive rate cycle and the joint effect of various geopolitical factors have pushed the Italian economy into stagnation mode. In the third quarter of 2023, GDP expanded a meagre 0.1% q/q, as the positive contribution of private consumption and net exports just outweighed the inventory drag.

Confidence data released over the fourth quarter has consistently signalled that industry was performing worse than services, and poor industrial production data for November offered hard evidence in support, suggesting that industry would be a growth drag in the fourth quarter.

“As services might not fully compensate, we are pencilling in a minor GDP contraction in 4Q23, confirming stagnation,” said ING in a note.

Notwithstanding flat economic growth, the labour market is resilient, confirming an effective hedge against short-run recession risks. In November, employment expanded by 0.1% on the month and 2.2% on the year. The pace of wage dynamics (hourly wages were growing by 2.7% YoY in November), while unspectacular, will help support real disposable income.

Spain: ING reports tentative signs that the slowdown in the Spanish economy is over and that growth may gradually accelerate this year. But, like in 2023, it will be characterised by a strong service sector while industry continues to languish.

Spain should see a gradual acceleration of economic growth in 2024. However, it will still be markedly held back, especially in the first half of the year, by the European Central Bank’s tighter monetary policy dampening investment and consumption, ING said in a note.

Tourism to Spain after the pandemic was the key driver to its recovery, giving it a solid lead over other eurozone countries early last year. The roll-out of European funds and the extension of some government support measures are also helping spur growth.

The European Sentiment Indicator also improved in its latest release. Spain was the only country to end the year above 100 points, including a 2.4-point rise in December.

The Netherlands: Encouraging household and public sector consumption was the main driver of the positive growth story for the Dutch economy in the last quarter of 2023. With below-2% inflation, high wage growth and government intervention, ING expects modest growth figures this year.

The recent contraction of the Dutch economy, which started in the first quarter of last year, may already have come to an end. October and November showed decent Month-on-Month growth in domestic household consumption, and consumer confidence rose for the fourth month in a row in December.

Contractual wage increase accelerated to 6.9% Year-on-Year while HICP consumer price inflation rate fell to 0.4% YoY in the fourth quarter (and core to 3.9%). That improvement in household consumption supports our view that the Dutch economy is looking rosier after three quarters of decline.

“That, combined with expanding public consumption, is expected to bring GDP growth into positive territory again in the last quarter of 2023, albeit at a sluggish pace due to weak exports and investment. This would mean that 2023 as a whole would have had an annual GDP growth rate of 0.1%, or in other words, “stagnation”,” ING said in a note.

Households, especially those with lower to middle incomes, will see gains in purchasing power in 2024, profiting from below-2% inflation combined with continuing high contractual wage growth of 4 to 6% and government interventions. This year, public spending is expansionary and remains a main driver of GDP growth.

Belgium: The Belgian economy is holding up well, with domestic demand so far having offset external trade weakness. Nevertheless, the first half of the year is likely to be difficult, and ING’s still awaiting a recovery in the manufacturing sector, ING said in a note.

Belgium’s industrial sector is suffering from weak demand and very high inventories of manufactured goods. As a result, the manufacturing sector has already lost 3.9% of activity since mid-2022. Belgian exports have fallen by more than 6% over the same period.

Restrictive monetary policy has led to a sharp slowdown in activity in the residential construction sector, with household investment in housing down by more than 11.5% since mid-2021.

“And yet, the Belgian economy continues to defy the laws of economics. Although the figure for the fourth quarter of 2023 is not yet available, GDP is expected to have grown by 1.4% in 2023, which is probably close to its potential,” ING said.

Several factors are contributing to the resilience of the Belgian economy: first, the automatic indexation of incomes has maintained household purchasing power more than elsewhere. Second, against all expectations, business investment has been growing strongly, which alone should contribute 1.4 percentage points to GDP growth in 2023. Third, fiscal policy in very accommodating although it resulted in the largest public deficit in the eurozone.

Portugal: One of the big drivers of growth, a further recovery in the tourism sector, will fall away this year. Combined with modest consumption dynamics, ING assumes average Portuguese growth will slow down this year, ING said in a note.

Portugal’s economy started 2023 strongly but slowed down sharply afterwards. The country still benefited from a further recovery in the tourism sector in the first few months of the year, but this positive effect on growth gradually faded throughout the year as visitor numbers rose back to pre-Covid levels.

“In the coming year, a recovery in real incomes through the combination of lower inflation and accelerating wage growth will support consumption, but several other factors will counter this positive effect,” ING said.

Although unemployment is still very low, business surveys show that hiring intentions among entrepreneurs are weakening. In addition, households will have to repay more on their loans due to rising interest rates, which will also dampen consumption. Some government measures which were introduced to support households against high inflation will also be abolished in 2024, further depressing consumption.

But growth is expected to rebound in the second half of the year on the back of a gradual easing of monetary policy and a pick-up in external demand.

“Overall, we expect the Portuguese economy to grow by 0.8% on average in 2024, which is above our euro area forecast but well below last year’s 2.1% growth. In 2025, we expect growth to accelerate again to 2.2%,” says ING.

Donald Trump Should Not Repeat Woodrow Wilson’s Failure

April 30th is an important date in American politics. This is the day 100 for the American President in the White House, and all attention will be on the reports of his achievements and failures. But nothing can be more critical than Peace…

○

6 mins read

A Holocaust perpetrator was just celebrated on US soil. I think I know why no one objected.

Russia’s invasion has made ordinarily outspoken critics of antisemitism wary of criticizing Ukrainian Nazi collaborators

○

1 min read

Qi Book Talk: The Culture of the Second Cold War by Richard Sakwa

Richard Sakwa has for many years been one of the most distinguished and insightful observers of relations between the West and Russia, and one of the leading critics of Western policy. In this talk with Anatol Lieven, director of the Eurasia program at the Quincy Institute, Sakwa discusses his book, The Culture of the Second Cold War (Anthem 2025). The book examines the cultural-political trends and inheritances that underlie the new version of a struggle that we thought we had put behind us in 1989. Sakwa describes both the continuities from the first Cold War and the ways in which new technologies have reshaped strategies and attitudes.